HELOCs: What They Are and How They Work

A HELOC, or Home Equity Line of Credit, is a revolving line of credit where you can use the current equity you have in your home and turn it into cash. It is a secured loan because it is backed by your home. A HELOC works similarly to a credit card, where you make monthly payments on what you spend. However, your monthly payments at first are only interest, it isn’t until a later date that you begin paying principal + interest.

Let’s Take a Closer Look at HELOCs

For the following examples, we are going to use a scenario where you own a home that is worth $200,000 and you still owe $50,000 on your mortgage.

How Much Can I borrow with a HELOC?

To start out with understanding HELOC, you need to understand equity. In relation to your home, equity is the difference between the appraisal value of your home and what you still owe on it from your primary mortgage (or the loan you initially used to purchase the home).

If your home is worth $200,000 and you still owe $50,000, the equity on your home is calculated by subtracting the amount owed from the value of the home.

$200,000 - $50,000 = $150,000

Now that we know what equity means, let’s dive into how that relates to HELOC. Depending on what financial institution you’re going to choose to finance your HELOC, you are only able to borrow a certain percentage of the appraisal value of your home. If you have a primary mortgage loan already, you’d subtract that to get the maximum amount of money you could borrow with a HELOC.

To calculate this, multiply the current value of your home by the percentage you can borrow (let’s say 85%), then subtract the amount you still owe from your primary mortgage. In this scenario, you can borrow a maximum amount of $120,000 through a HELOC.

($200,000 * 85%) - $50,000 = $120,000

transfer to your checking account. You also may have the opportunity to open a HELOC account card, where you can track your HELOC expenses as separate from other expenses. The period that you can spend and use the HELOC money is called the draw period.

Timeline of a HELOC

The timeline of a HELOC is separated by a draw period and a repayment period. Traditionally, the draw period for a HELOC is 10 years. During this time, you can use money from your HELOC as you wish while only paying monthly interest. Once the draw period finishes, you can no longer borrow money from the home equity and the repayment period begins.

You will pay interest + principal monthly until the end of the repayment period. Once you have repaid the principal and interest, the HELOC as a whole comes to an end.

HELOC Rates

Depending on the lender you work with, they’ll offer either fixed or variable rates. It is most common for HELOCs to have a variable rate since all HELOC rates fluctuate periodically, as they are based on the Wall Street Journal Prime Rate.

Your loan-to-value (LTV) percentage and combined loan-to-value (CLTV) percentage also play a factor in determining what your rate will be. It’s important to note that numbers will vary from lenders on how much you can borrow; always do your research beforehand.

HELOC Qualifications

HELOCs are a great option for many people and are simple to apply for online. However, if you want to borrow a higher amount of money with a HELOC, you must meet a couple of qualifications to assure the lender you’re a good loan candidate.

Let’s look more into these qualifications:

Credit Score

Your credit score will affect how much you are able to borrow. The higher the score, the more you’ll be able to borrow. If your credit is on the low end, you may be limited in the amount you can borrow. Perhaps only $80,000 of that $120,000.

If you have a low credit score and are considering a HELOC, it might be worth thinking about other options; perhaps waiting until your credit score improves or taking out a smaller, different type of loan.

Debt-to-Income Ratio

Another aspect that lenders consider is your debt-to-income ratio or DTI. In other words, the total amount of monthly payments owed on all outstanding credit debts, vs. total income. These debts could be from student loans, car payments, or any loan you are required to pay monthly.

Calculate your DTI by taking your total monthly debt and dividing it by your total monthly income. If your debt is $1,500 every month and you bring in $4,000 every month, your DTI is in great shape.

($1,500 ÷ $4,000) = 37.5% DTI

Lenders usually like to see your DTI be less than 42%. The lower your DTI percentage is, the better. Lenders look at this number to see how many other monthly payments you already currently have. This helps lenders determine if you can afford another monthly loan payment.

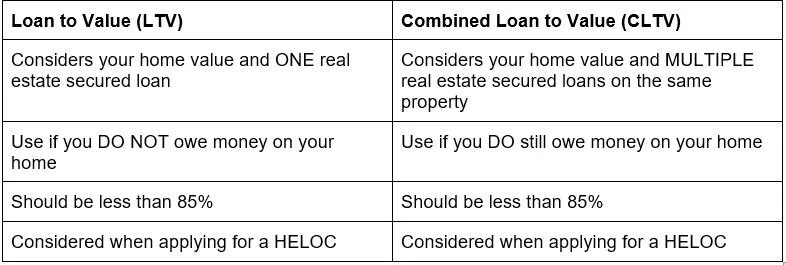

Loan-to-Value Ratio

Your loan-to-value ratio, or LTV, is also considered when applying for a HELOC loan. To calculate this, we would take the current loan amount and divide it by the current appraisal value of your home. A homeowner with a $50,000 mortgage and a home appraised at $200,00 would have an LTV of 25%.

($50,000 ÷ $200,000) = 25% LTV

If you don’t owe anything on your $200,000 home mortgage and want to take out a $70,000 HELOC, you’d divide the amount you wish to borrow by the value of your home. Lenders like to see LTVs less than 85%.

($70,000 ÷ $200,000) = 35% LTV

Combined Loan-to-Value Ratio

The difference between LTV ratios and combined loan-to-value ratios, or CLTV, is that the LTV considers only the value of your home + one other value. While a CLTV factors in the value of your home + multiple other values.

Again, let’s say you have a $200,000, still owe $50,000, and wish to take out a $70,000 HELOC. Your CLTV ratio would be calculated by adding your current mortgage with the desired amount of HELOC, then dividing that number by your home’s appraisal value. Lenders look for an LCTV of 85% or less.

($50,000 + $70,000) ÷ $200,000 = 60% CLTV

Use the chart below as a helpful guide:

When to Consider a HELOC

Consider if what you’ll be using your HELOC for makes sense. Remember, you are using your home as collateral; you risk losing your home if you cannot pay the principal and interest.

HELOCs are ideal for those doing home renovations to increase the value of their home. Especially considering a $10K renovation could easily increase home value by double that amount!

Home Equity Loans vs. HELOCs

There are a few major differences between a home equity loan and a HELOC.

Money Distribution

· Home Equity Loan - You receive all the money at once, a lump sum payment at the time of closing, or within a short period of time after the loan closing.

· HELOC - Works like a credit card rather than a cash payment.

Payment Period

· Home Equity Loan - Start paying back the principal and interest right away.

· HELOC - Pay interest and principal in two periods: interest first, then the principal.

Payment Amount

· Home Equity Loan - Pay interest + principal for the full amount borrowed.

· HELOC - Only pay interest + principal of the money used, not the HELOC amount.

Interest Rates

· Home Equity Loan - Typically have fixed rates so you’ll always know the amount owed.

· HELOC - Typically have variable rates (based on Wall Street Journal Prime Rate). Rates may go up or down over the period of the HELOC.

Explore a HELOC with Together CU

Check out the HELOC options that we offer here at Together Credit Union, or any of our loan options. We’ll help you find the best fit. You can apply for a HELOC online or make an appointment in person with us today. We’re here for you!